We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

US Treasury Yields Rise amid Uncertainty on US-Iran Talks

July 1, 2026

US Treasury yields inched higher by 7-9bp across the curve. Technical talks between the US and Iran are said to have continued yesterday, but without any high-level meetings. Following uncertainty regarding the status of the negotiations, crude oil prices inched higher. On the data front, the Conference Board Consumer Confidence Index came-in at 91.2, softer than expectations of 94.4.

Looking at US equity markets, the S&P and Nasdaq ended higher by 0.8% and 1.5% respectively. US IG CDS spreads were wider by 0.3bp and HY CDS spreads widened by 3.3bp. European equity markets ended higher. European IG CDS spreads were 0.3bp tighter, while Crossover spreads tightened by 2.2bp. Asian equity markets have opened mostly higher this morning. Asia ex-Japan CDS spreads were trading stable. China’s official manufacturing PMI rose to 50.3 in June, beating expectations of 50.1.

Rating Changes

- Airbus SE Upgraded To ‘A+’ On Solid Financial Flexibility, Outlook Stable; Debt Ratings Raised To ‘A+’

- Fitch Places Comcast Corp. on Rating Watch Negative

- Fitch Revises Martin Marietta’s Outlook to Negative on LNA Acquisition; Affirms IDR at ‘BBB+’

Term of the Day: American Depositary Receipts (ADRs)

ADRs are USD-denominated certificates that trade on American stock exchanges and track the price of a foreign company’s domestic shares. They trade like regular US stocks and can represent a single share, multiple shares, or a fraction of a share of the foreign stock. They offer portfolio diversification and convenient trading during US market hours. However, unlike common stock, ADRs do not grant investors ownership rights.

SK Hynix recently announced plans to raise up to $29.4bn via a Nasdaq listing of American Depositary Receipts (ADRs).

Talking Heads

On AI Leverage Is More Worrying Than Valuations – Tobias Adrian, IMF

“What is quite worrisome from a financial stability perspective is that the major tech firms are starting to leverage up themselves. There’s a potential maturity mismatch in between the duration of the physical assets and the duration of the debt… There’s not as much valuation pressure anymore that you saw recently”

On Treasury Market’s June Rally Bails Out Quarter and First Half

John Briggs, Natixis North America

“The second quarter for rates was an eventful one to say the least”

Priya Misra, JPMorgan Asset Management

“The last three months were all about trying to separate the signal from the noise… evidence of inflation spillover from oil into broader inflation metrics, and is the labor market reaccelerating”

Ian Lyngen, BMO Capital Markets

“Rebalancing flows have been particularly topical this quarter given the relative performance of equities versus fixed-income”

On ‘Explosive’ Dollar Rally Is Among Biggest Pain Trades – HSBC

“A stronger dollar would be painful, but we see the ‘pain trade’ in the FX market taking the form of a more explosive period of USD strength… Though positioning in flatteners may not be quite as crowded as steepeners were at the start of the year, we think curve steepening would now represent a pain trade for markets”

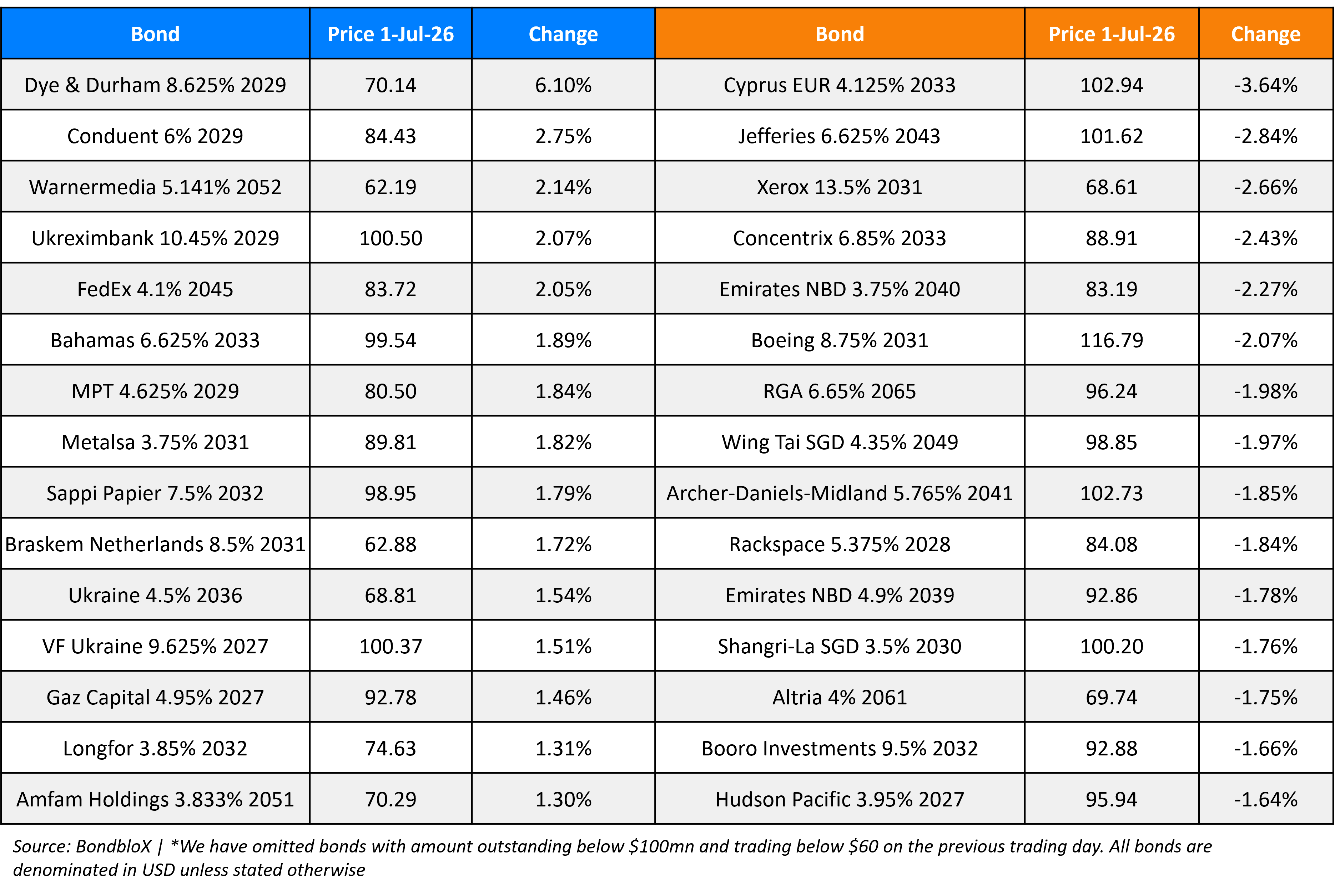

Top Gainers and Losers- 01-Jul-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.