We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

US Treasury Yields Eased Again Following PPI Print

July 16, 2026

US Treasury yields eased again on Wednesday, following an easing in the producers prices inflation prints. US Headline PPI for June came in at 5.5%, softer than expectations of 6.2%. Core PPI came in at 4.7%, again softer than expectations of 5.1%. New York Fed President John Williams said that the current stance of monetary policy is well positioned to bring inflation back toward the 2% goal, adding that he saw encouraging reasons to expect that inflation has peaked.

Looking at US equity markets, the S&P and Nasdaq rose by 0.4% and 0.6% respectively. US IG CDS spreads were 0.8bp tighter and HY CDS spreads tightened by 3.2bp. European equity markets ended lower. European IG CDS spreads were 0.3bp tighter, and Crossover spreads tightened by 2.2bp. Asian equity markets have opened mixed this morning. Asia ex-Japan CDS spreads were 1bp tighter.

Rating Changes

- Moody’s Ratings upgrades KeyCorp (issuer rating to Baa1 from Baa2); Outlook Stable

- Fitch Revises MasterBrand’s Outlook to Negative; Affirms IDR at ‘BB+’

- Commerzbank AG Outlook Revised To Stable On UniCredit Takeover Progress; ‘A/A-1’ Ratings Affirmed

Term of the Day: Subordinated Bonds

Subordinated bonds refer to bonds that rank below senior debts on the capital structure. In the event of liquidation, holders of subordinated debt would only be paid after all the senior debt is repaid. Thus, the ratings and yield of subordinated debt tend to be lower and higher respectively, to account for the greater risk associated with subordinated vs. senior debt. There are different kinds of subordinated debt that can include perpetuals/AT1 CoCos, payment-in-kind notes, mezzanine debt, convertible bonds, vendor notes etc. Subordinated debt rank higher to preferred equity and common equity in the capital structure.

Talking Heads

On prepared to act soon if inflation does not begin to slow – Lisa Cook, Fed Governor

“I see it as prudent to give a bit more time to observe how inflation unfolds from here. Going forward, though, I believe the risks continue to be strongly weighted toward higher inflation… If we do not see signs of disinflation soon, I am prepared to act. I am fully committed to reaching our inflation target, and this commitment is unwavering.”

On Favoring 5- to 10-Year Treasuries as Fed Turns Quiet – Andrew Balls, Pimco

“I’d say across the curve, five- to 10-year part of the curve looks pretty good… The level of nominal yields, real yields, is very attractive… From my point of view, not providing a lot of forward guidance is perfectly sensible.”

On Colombia’s Tiger Trade Is Powered by High Rates, Fiscal Optimism

David Austerweil, VanEck

“Colombia sovereign credit spreads are the tightest they have been post-Covid, while local yields are still elevated even relative to recent history, so they are more attractive”

Arif Joshi, Bramshill Investments

“We are positioned in local debt unhedged because we think the new administration has a credible target and both rates and the peso will benefit”

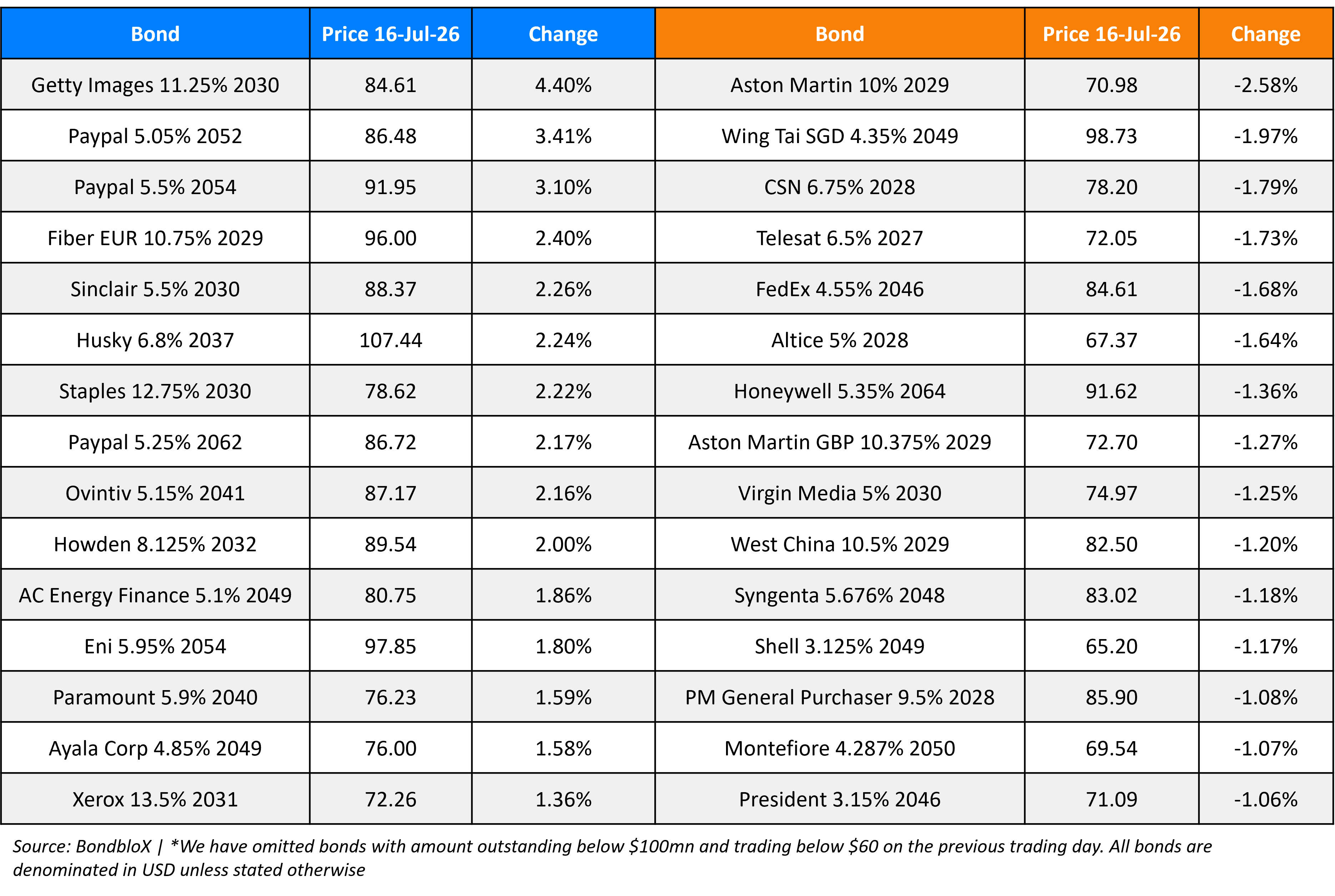

Top Gainers and Losers- 16-Jul-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.