We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

US Treasury Curve Flattens; Markets Continue to Price in Possibility of a Fed Hike

May 25, 2026

The US Treasury yield curve flattened on Friday. On the data front, the final reading of the University of Michigan consumer sentiment index for May came-in at 44.8, a record low, falling for a third consecutive month. On the geopolitical front, US President Donald Trump said that he will not “rush” into an agreement with Iran, adding that a peace agreement has been “largely negotiated”. However, reports indicated that Iran has no optimism about an agreement.

Looking at equity markets, the S&P and Nasdaq ended higher by 0.4% and 0.2% respectively. US IG CDS spreads tightened by 0.4bp and HY CDS spreads were 2.1bp tighter. European equity markets ended in the green. The iTraxx Main CDS spreads were 1.8bp tighter and Crossover spreads tightened by 6.3bp. Asian equity markets have opened in the green this morning. Asia ex-Japan CDS spreads were flat.

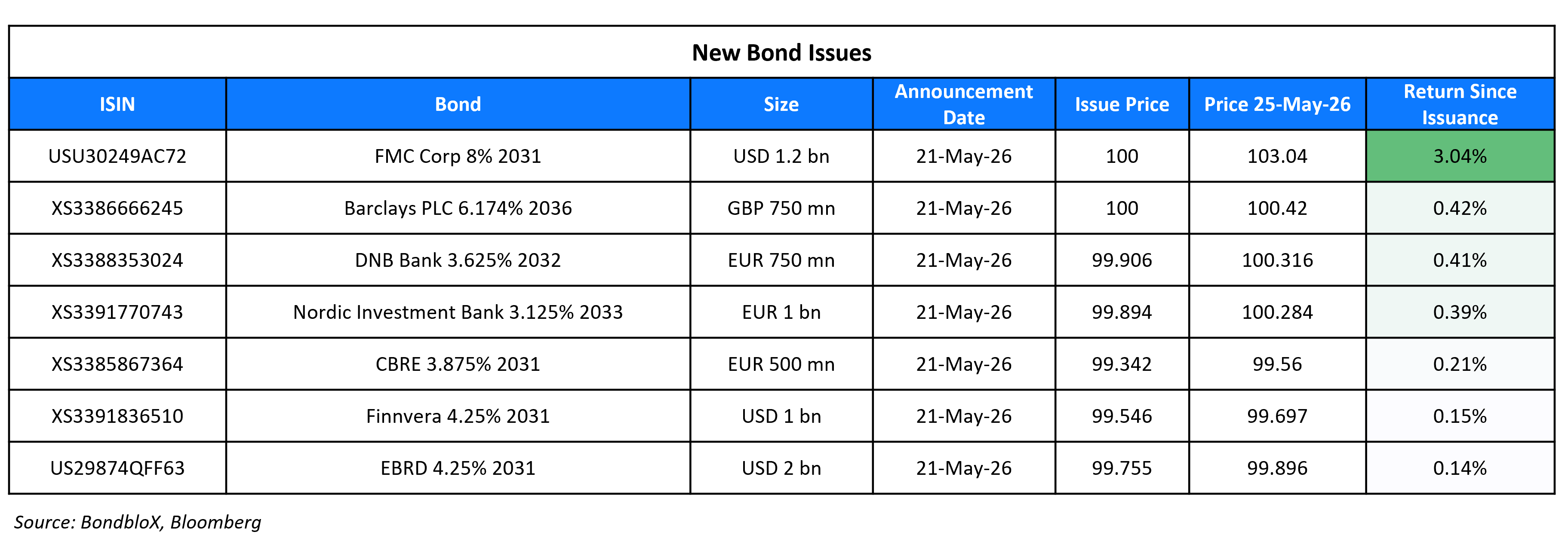

New Bond Issues

Rating Changes

- Kioxia Upgraded To ‘BBB-‘ As Earnings and Finances Improve Beyond Expectations; Outlook Stable

- Seplat Upgraded To ‘B+’ Following Similar Action On Nigeria

- Moody’s Ratings upgrades Scentre’s hybrid notes to A3 and affirms A2 ratings; outlook stable

- Fitch Downgrades SJM Holdings to ‘B+’; Outlook Stable

- Fitch Revises Frontier Clearing Corporation’s Outlook to Negative; Affirms IFS Rating at ‘A-‘

- Moody’s Ratings takes action on Mexican corporates following sovereign rating action

Term of the Day: Convexity Hedging

Convexity hedging refers to a phenomenon of hedging portfolio interest rate exposure through bonds that stand to get impacted due to duration and convexity changes. This is most commonly used in mortgage-backed securities (MBS), given the prepayment profiles. For example, when interest rates rise, MBS investors would see their portfolio duration rise (as prepayments slowdown) and therefore they would have to cut their exposure to high duration securities – predominantly longer-dated Treasuries and swaps to keep duration levels aligned with the benchmark. Thus for example, if rates rise, principally MBS duration rises and Treasury duration falls thus changing the hedge ratio of MBS vs. Treasuries – effectively having to sell more Treasuries than otherwise to hedge their MBS portfolios.

Vishal Khanduja from Morgan Stanley Investment Management said, “The velocity of the move in yields has been concerning and we have seen some forced selling because of convexity hedging”.

Talking Heads

On Fed Will Act on Inflation as Yields Spike – Dan Ivascyn, Pimco

If long-dated inflation expectations “become more significantly unanchored, then you are going to see a tightening of policy even in the face of some economic weakness…That’s the pain trade for markets”

On Repeated Supply Shocks Test Inflation Anchor – Thomas Barkin, Richmond Fed President

“With inflation above our 2% target for over five years now, it’s worth asking whether the cumulative impact of so many waves risks loosening the anchor… it comes down to how much businesses, consumers, and inflation expectations can take.”

On Yield Curves May Steepen Further in Key Southeast Asian Markets

George Efstathopoulos, Fidelity International

“Markets with weaker fiscal buffers or greater energy import dependence are likely more exposed to steepening risk, which means Asean markets seem most vulnerable should oil prices stay higher for longer”

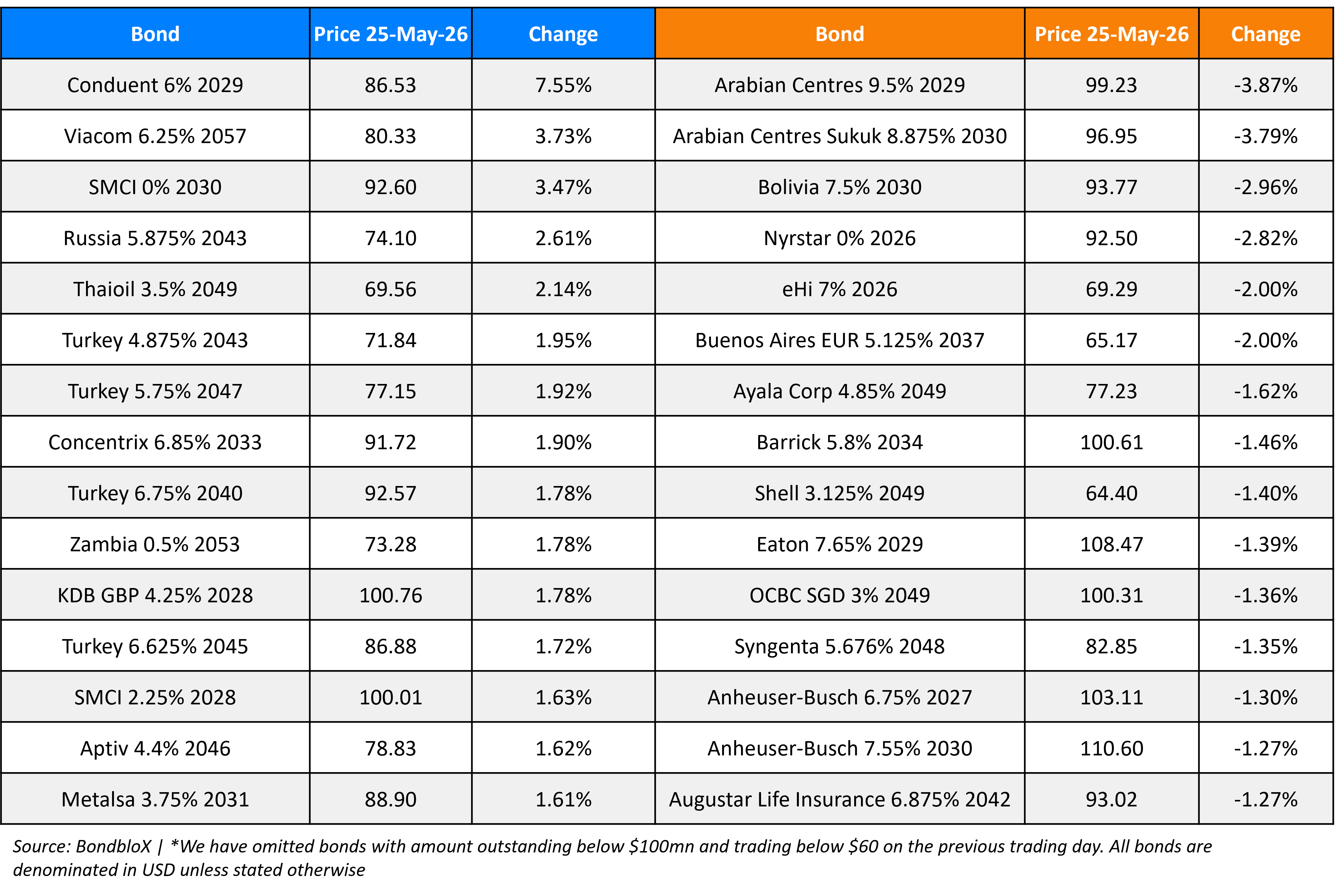

Top Gainers and Losers- 25-May-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.