We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

US Treasury Yields Drop as June Inflation Eases

July 15, 2026

The US Treasury curve bull steepened, with the 2Y yield moving lower by 8bp while the 10Y was 2bp lower. This came after an easing in the inflation print. US Headline CPI for June came in at 3.5%, softer than expectations of 3.8% and the prior month’s 4.2% print. Core CPI came in at 2.6%, again softer than expectations of 2.8% and the prior month’s 2.9% print. Fed Chairman Kevin Warsh committed to the 2% inflation objective in his testimony to the House Financial Services committee. Chicago Fed President Austan Goolsbee said that the June inflation reading was surprisingly benign, but would want several months of easing prints.

Looking at US equity markets, the S&P and Nasdaq rose by 0.4% and 0.9% respectively. US IG CDS spreads were 0.3bp tighter and HY CDS spreads tightened by 2.6bp. European equity markets ended higher. European IG CDS spreads were 0.2bp wider, and Crossover spreads widened by 2.1bp. Asian equity markets have opened in the green this morning. Asia ex-Japan CDS spreads were 1.5bp wider.

Rating Changes

- Fitch Upgrades Capex’s LC IDR to ‘B’; Affirms FC IDR at ‘B-‘

- Moody’s Ratings upgraded Carlisle’s senior unsecured rating to Baa1; outlook stable

- Carpenter Technology Corp. Outlook Revised To Positive On Strong Earnings And Low Leverage; ‘BB+’ Ratings Affirmed

Term of the Day: Bull Steepening

Bull Steepening refers to a change in the yield curve where short-end rates move down faster than long-end rates. This not only has a steepening effect on the entire yield curve but also has a net effect of interest rates moving lower and bond prices moving higher.

Similar terms include Bear Steepening, Bull Flattening and Bear Flattening. If the yield curve moved lower and bond prices moved higher, it is considered a bull move, while the opposite is a bear move. If the effect of the move is to steepen the curve, it would either be a Bear Steepening or a Bull Steepening. If the effect was to flatten the curve, it would be a Bear Flattening or Bull Flattening.

Talking Heads

On Fed Behind The Curve as Tech Economy Booms – TS Lombard

“There are so many different types of shocks hitting the economy — that’s why it’s quite hard to tell how far behind the curve they are. We probably are in an environment where this economy can sustain higher interest rates… Interest rates should be even higher to sort of curtail the buildup of leverage in that new tech economy.”

On Emerging Bond Returns Beating Treasuries as Carry Trades Boom

Brad Godfrey, Morgan Stanley Investment Management

“After a brief pause around the start of the conflict, investors are still seeking to diversify their overweights to US capital markets. We believe flows into EM debt should be very supportive.”

Kamakshya Trivedi, Goldman Sachs

“It speaks to this new emerging resilience. The improved fundamentals — are all contributing to it “

Wei Li, BlackRock

“We see a more attractive risk-reward profile in EM local debt. We like the yield relative to its volatility and improving fundamentals”

On Japan’s Bid to Bring Money Home Faces Fiscal, BOJ Reality Check

Laura Cooper, Nuveen

“While it shows the market is eager to add duration… there needs to be greater clarity on the fiscal and rate-hiking paths”

Jane Foley, Rabobank

“It does appear that the Ministry of Finance is exploring ways of supporting the yen beyond intervention. But the government will still need to provide greater reassurance on fiscal policy”

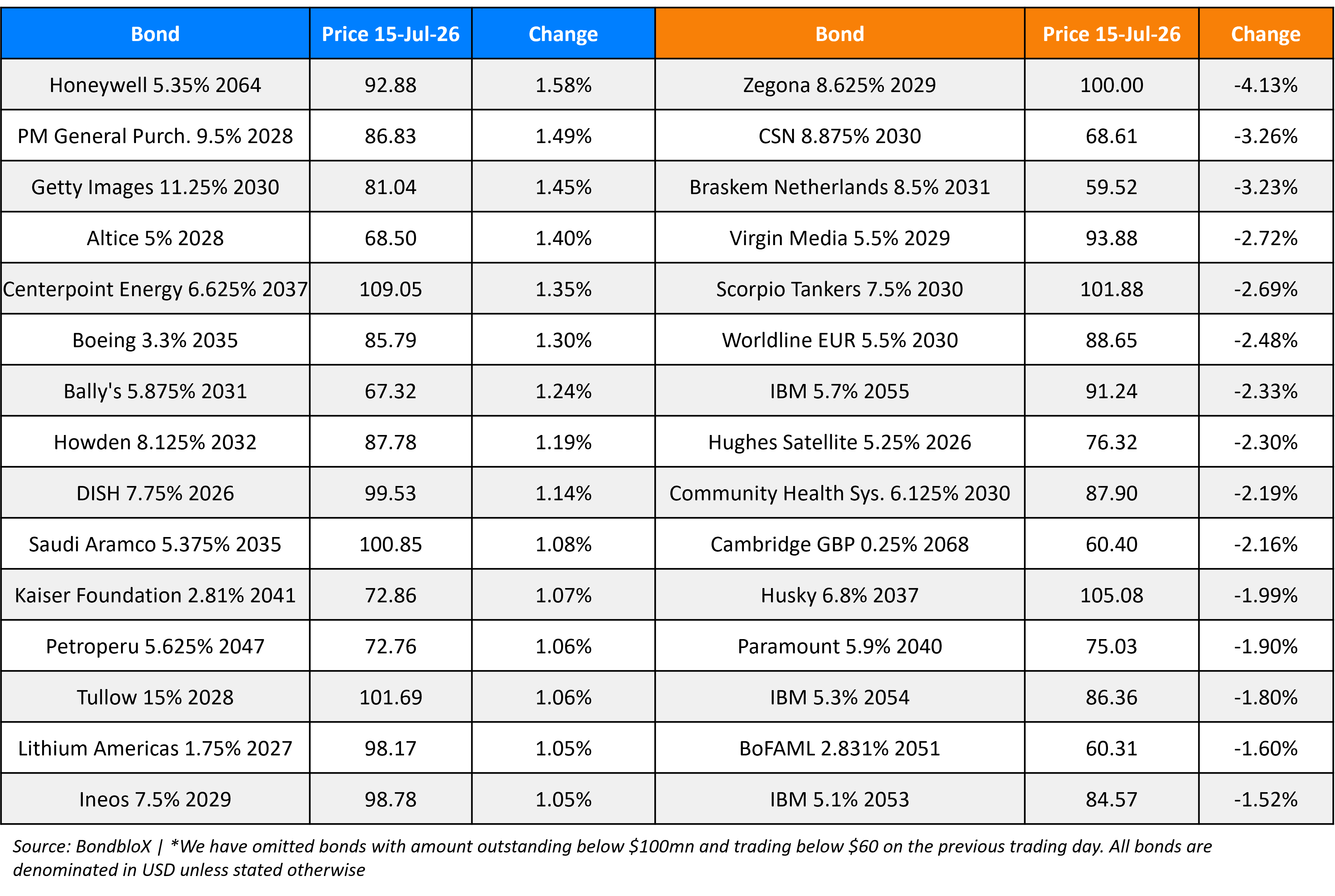

Top Gainers and Losers- 15-Jul-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.