We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Sea of Red in Global Markets; Treasury Yields Soar to Highs

May 18, 2026

US Treasury yields soared higher across the curve – the 2Y and 10Y yields are at their highest levels since the beginning of 2025, while the 30Y is at 5.16%, levels last seen in 2007. Markets are now pricing-in nearly 17bp in Fed rate hikes by the end of the year amid concerns about inflationary pressures. Besides, US President Donald Trump warned that “the clock is ticking” for Iran and that “they better get moving, fast, or there won’t be anything left of them”.

Equity markets saw a sea of red. The S&P and Nasdaq ended lower by 1.2% and 1.5% on Friday. US IG CDS spreads widened by 0.8bp and HY CDS spreads were 8bp wider. European equity markets ended sharply lower too. The iTraxx Main CDS spreads were 1.7bp wider and Crossover spreads widened by 8.5bp. Asian equity markets have opened in the red this morning. Asia ex-Japan CDS spreads were 2.8bp wider.

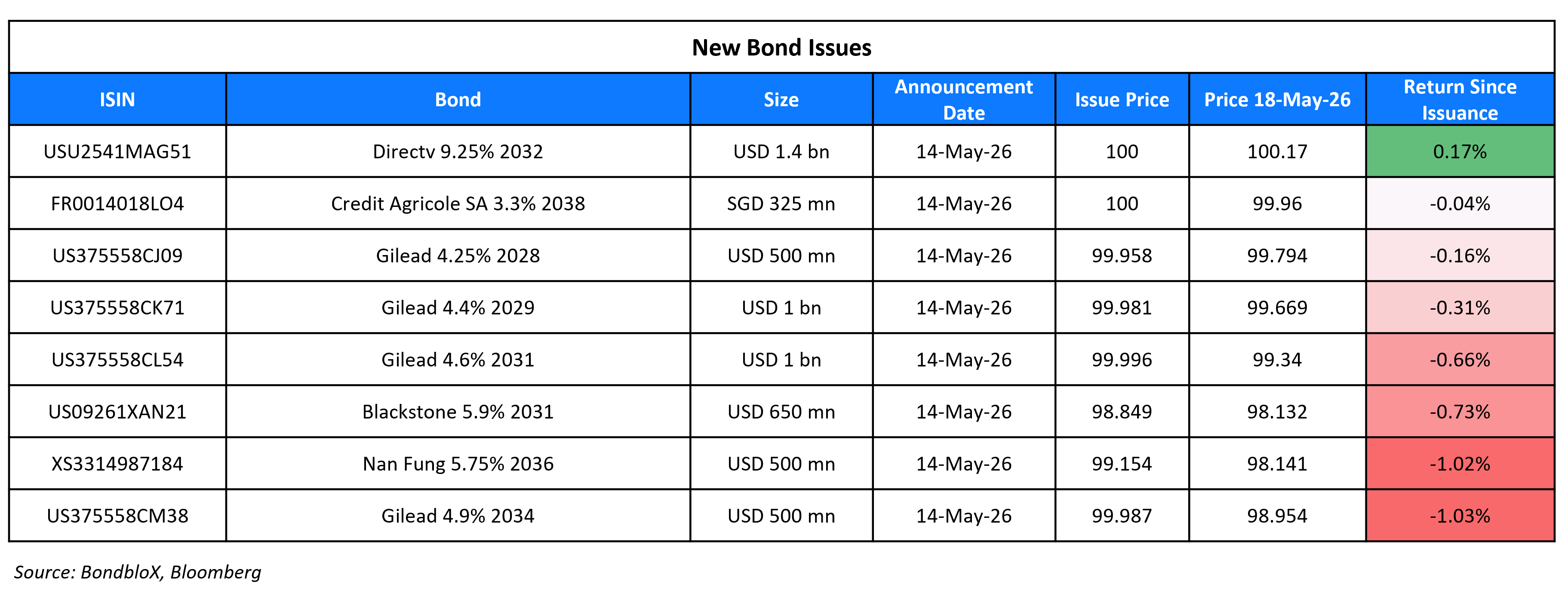

New Bond Issues

- OCBC $ 3Y at SOFR+80bp area

- Korea Credit Guarantee Fund $ 3Y at T+70bp area

New Bonds Pipeline

- Republic of Congo offshore bond

Rating Changes

- Fitch Upgrades Teva’s Long-Term IDR to ‘BBB-‘; Outlook Stable

- Nigeria Upgraded To ‘B’ From ‘B-‘ On Improving Macroeconomic Profile; Outlook Stable

- Ipoteka Bank JSCM Upgraded To ‘BB’ On Strengthening Capitalization; Outlook Stable

- Moody’s Ratings downgrades SJM’s CFR to B1; changes outlook to stable

- Bulgaria Outlook Revised To Positive On Improved Political Stability And Modest Government Debt

- Fitch Revises Goldman Sachs BDC’s Outlook to Negative; Affirms at ‘BBB-‘

Term of the Day: Debtor-in-Possession (DIP) Financing

Debtor-in-possession (DIP) Financing is a funding option available to distressed companies that have filed for Chapter 11 bankruptcy protection, where lenders believe that the company has a realistic chance of turning itself around. DIP financing is not an option available to distressed companies that simply want to liquidate the company. DIP financing can be a lifeline for distressed companies as it may find it hard to borrow from typical channels after filing for Chapter 11.

From a lender’s perspective, DIP financing can be attractive given the special treatment of such financing under US bankruptcy laws, which dictate that DIP lenders are to be paid before other creditors. DIP financing is subject to court approval wherein the distressed borrower must prove to the courts that the existing or older creditors will not be made worse by the new financing.

Talking Heads

On Not Possible for the Fed to Cut Rates – Jeffrey Gundlach, DoubleLine

“People were looking for two rate cuts this year, but the inflation market has simply not cooperated… just not possible, in my view, to cut interest rates when the two-year Treasury is almost 50 basis points higher than the Fed funds rate”

On Bond Traders Seeing Shift Toward New Era of Higher Yields

Priya Misra, JPMorgan Asset Management

“This price action is concerning for two reasons – Long-end rates are rising globally which tend to feed on each other, and the prospect of Fed hikes is coming into the market narrative”

Karen Manna, Federated Hermes

“We are seeing a world that’s really reckoning with renewed inflation”

Kevin Flanagan, WisdomTree

“There is a sense that the bond market is requiring more of a concession to own new Treasuries in this environment… inflation narrative is dominating the market”

On G-7 to Discuss Bond Selloff as Yields Hit Multi-Decade Highs

Scott Bessent, US Treasury Secretary

“There’s been a global backup in bond yields as markets are pricing in, perhaps, inflation — a short term blip in inflation — that I believe is transient”

Satsuki Katayama, Japanese Finance Minister

“Bond yields have been rising across all three major markets. These developments are interacting with each other and creating something of a compounding effect.”

Top Gainers and Losers- 18-May-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.