We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

ISM Services PMI Meets Expectations

July 7, 2026

US Treasury yields were broadly stable across the curve. The ISM Services PMI reading came in at 54.0 in June, inline with expectations. Among the sub-components, the Prices Paid Index and New Orders Index decelerated, while the Employment Index jumped to expansion territory after seeing a contraction in May.

Looking at US equity markets, the S&P and Nasdaq rose by 0.7% and 1.1% respectively. US IG CDS spreads were 0.7bp tighter and HY CDS spreads tightened by 3.7bp. European equity markets ended lower. European IG CDS spreads were 0.2bp tighter, and Crossover spreads tightened by 1.9bp. Asian equity markets have opened mostly lower this morning. Asia ex-Japan CDS spreads were 0.1bp tighter.

Rating Changes

- Fitch Upgrades JSW Steel to ‘BB+’; off Rating Watch Positive; Outlook Positive

- Moody’s Ratings downgrades OHI’s ratings to B3; outlook negative

- Suzano S.A. ‘BBB-‘ Ratings Affirmed After Conclusion Of Joint Venture With Kimberly-Clark; Outlook Remains Positive

- Shanghai Electric Holdings, Subsidiary Outlook Revised To Positive on Strengthening Cash Flow; ‘BBB+’ Ratings Affirmed

Term of the Day: Earnouts

Earnouts are a contractual provision during a merger or acquisition, providing for contingent additional payments from the buyer of a company to the seller’s shareholders. Essentially, earnouts state that the seller of a business would receive compensation in the future if the merged/acquired business achieves certain financial goals. Earnouts help bridge the differing views that both parties may have regarding the M&A agreement on an upfront cash price or valuation for example.

Talking Heads

On Peace Deal Not Restoring Pre-War Situation – Isabel Schnabel, ECB

“Does the decline in oil prices mean that we are back to the pre-war situation? I don’t think so. The peace deal is still fragile. Markets continue to point to higher oil prices over longer horizons. Gas prices are still around 40% higher than before the war”

On ‘Forward Guidance’ Needs to Be Flexible – Christopher Waller, Fed Governor

“I continue to believe that forward guidance can be a valuable tool that has, at times, significantly strengthened policymaking and will continue to be useful. But forward guidance is more art than science, and there have been times when it has hindered, rather than helped, policymaking.”

On Wall Street Warming to India’s Markets as Oil Pressures Fade

K. Balasubramanian, Citigroup

“The 18-month long negative cycle on India is eclipsing fast. Investor sentiment is on the cusp of changing. They are beginning to think about India, with the fiscal deficit narrowing and the rupee coming out of the rout loop.”

Steven Holden, Copley Fund Research

“Given the concentration risk sitting in Taiwan and South Korea, it’s hard to imagine active EM managers not rotating back into China and India”

Barclays economists

“The economy that was too expensive a year ago is now available at a meaningful discount while still growing near 7%”

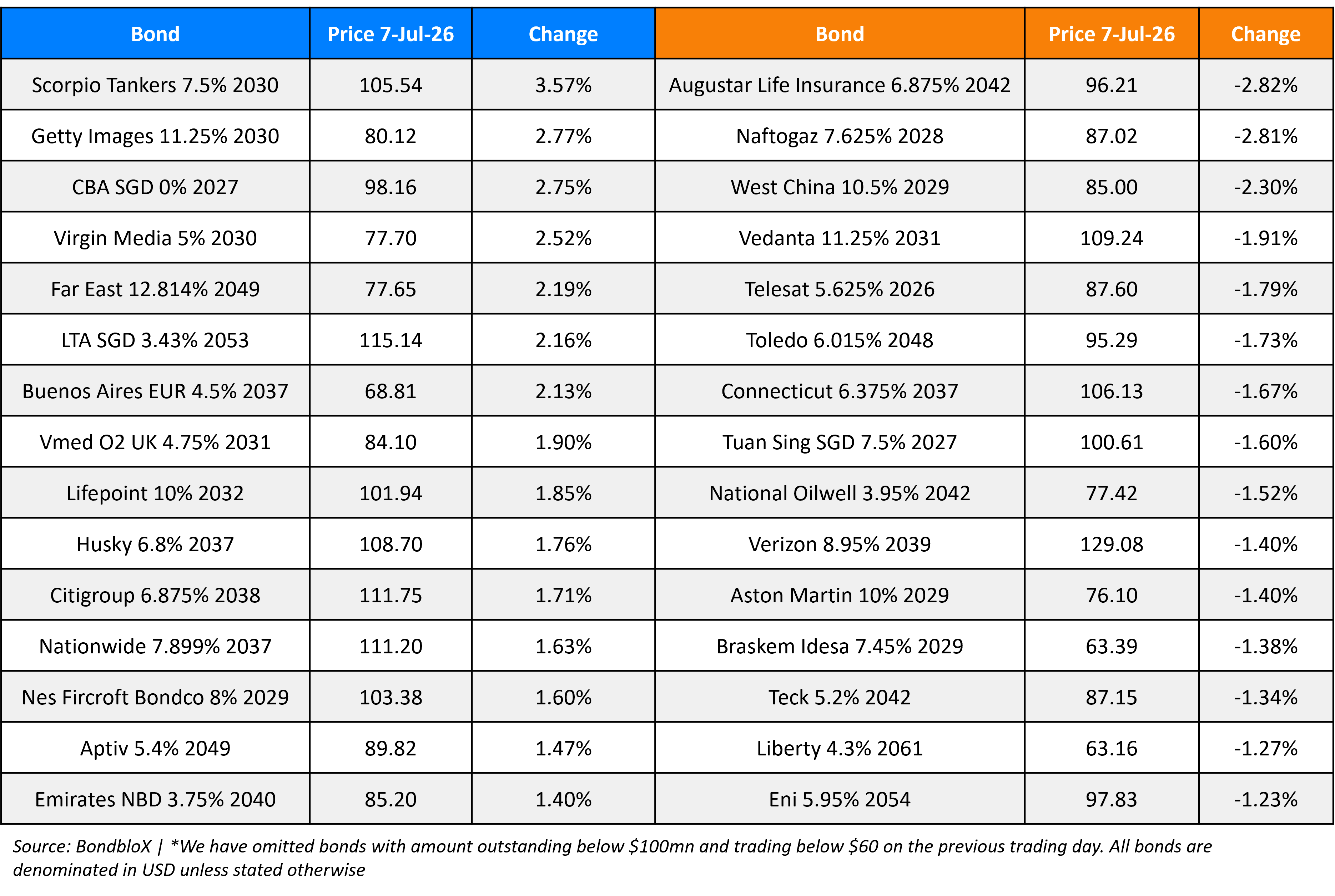

Top Gainers and Losers- 07-Jul-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.