We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

HSBC Launches $ PerpNC7; US Jobs Report Beats Expectations

May 11, 2026

US Treasury yields remained nearly unchanged. On the data front, NFP for April showed a rise of 115k jobs, coming in much higher than estimates of a 65k gain. The NFP print for March was revised higher to 185k from 178k priorly. Average Hourly Earnings (AHE) YoY rose by 3.6%, higher than the surveyed 3.8%. The Unemployment Rate stood at 4.3%, inline with expectations. On the geopolitical front, US President Donald Trump rejected Iran’s response to their proposal for peace talks, terming it as “totally unacceptable”.

Looking at US equity markets, the S&P and Nasdaq ended higher by 0.8% and 1.7% respectively. US IG CDS spreads were 0.7bp tighter and HY CDS spreads were 4.5bp tighter. European equity markets ended lower. The iTraxx Main CDS spreads were flat and the Crossover spreads tightened by 1.1bp. Asian equity markets have opened broadly weaker this morning. Asia ex-Japan CDS spreads were 0.3bp tighter.

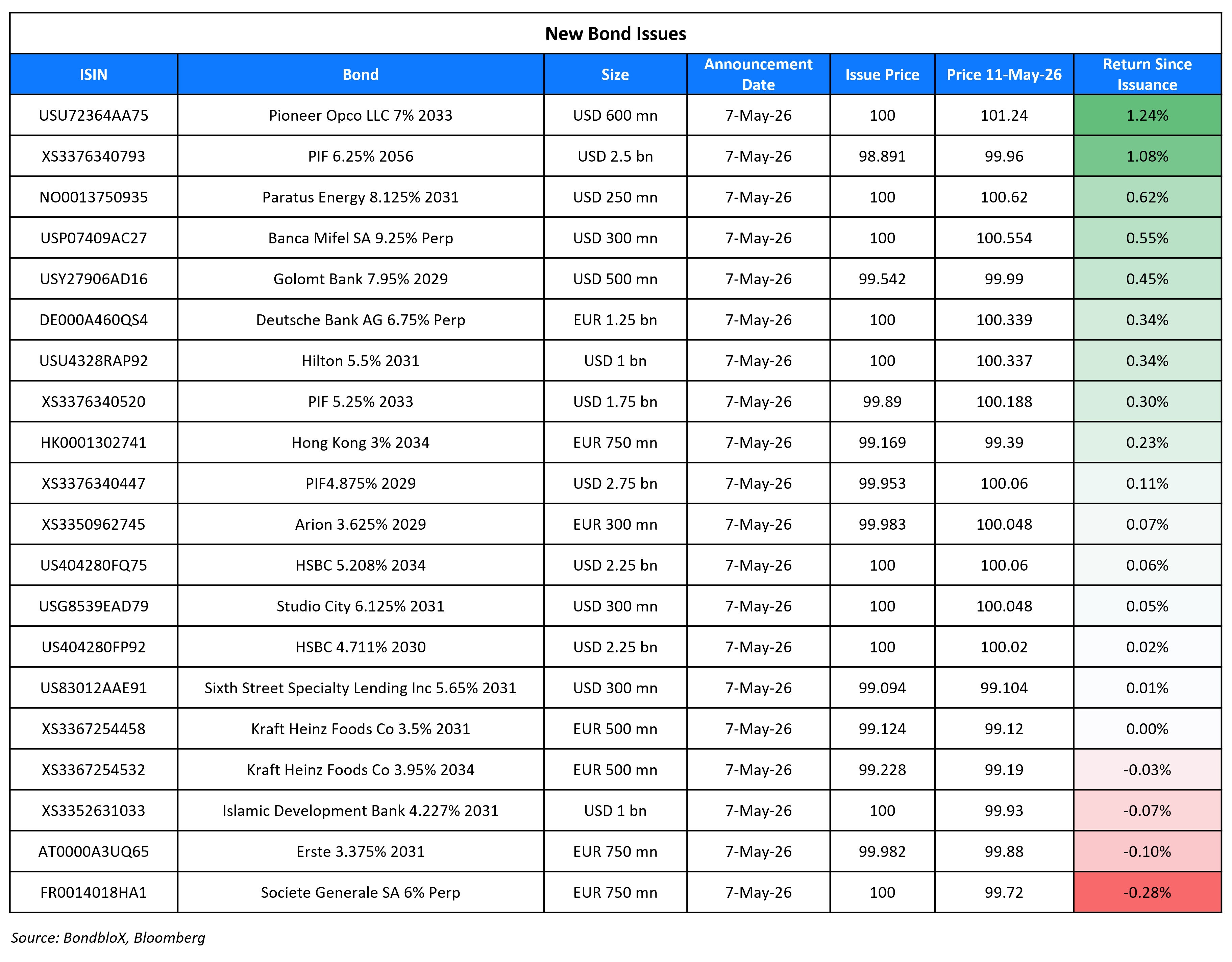

New Bond Issues

- HSBC $ PerpNC7 AT1 at 7.25% area

- OUE Treasury S$ 7Y at 3.5% area

- ICBC Finance Leasing 3Y FRN at SOFR+105bp area

- Bank of China Panama $ 3Y FRN at SOFR+90bp area

Rating Changes

- Moody’s Ratings upgrades Shriram Finance’s rating to Baa3 from Ba1; outlook stable

- Fitch Upgrades Ghana to ‘B’; Outlook Positive

- Tullow Oil PLC Upgraded To ‘CCC+’ On Refinancing; Outlook Stable; New Senior Secured Notes Rated ‘CCC+’

- Moody’s Ratings upgrades Bermuda’s ratings to A1, maintains stable outlook

- Fitch Upgrades Phoenix Aviation Capital LLC to ‘B+’; Outlook Stable

- Grupo Televisa Downgraded To ‘BBB-‘ From ‘BBB’ On Weaker RGUs And Market Share; Outlook Negative

- Fitch Places Frontera’s Senior Notes on Rating Watch Positive

Term of the Day: Non-Farm Payrolls (NFP)

Non-Farm Payrolls (NFP) is a key data point that is released by the US Bureau of Labor Statistics (BLS) usually on the first Friday of every month. NFP measures net changes in employment excluding agricultural, local government, private household and not-for-profit sectors over the past month and is a key economic indicator in the United States. A high reading of the NFP is considered a positive sign for the US economy while a negative reading is considered a sign of a slowdown in the US jobs market. The NFP indicator is closely watched by traders, especially as it is one of the first monthly economic indicators to be released, and because of the direct relationship between job creation and economic growth.

Talking Heads

On Seeing Risk of Fed Hiking Rates Due to Iran War – Dan Ivascyn, Pimco CIO

“US is further away from that, but you are going to see more tightening as it looks today in Europe, the UK and maybe even Japan, and I wouldn’t take it completely off the table for the US either”

On Seeing Fed Cuts Delayed to December, March on Inflation – Goldman Sachs

Push back expectations for Fed’s next two rate cuts by one quarter to December 2026 and March 2027… “A combination of lower monthly inflation prints after the oil shock fades and further labor market softening will likely be needed”

On ECB Torn Between Risk of Acting Too Early, Too Late – Christine Lagarde, ECB President

“We are constantly torn between the risk of reacting too quickly or the risk of reacting too late, and we have to find the right path to navigate our economies toward that 2% medium term inflation”

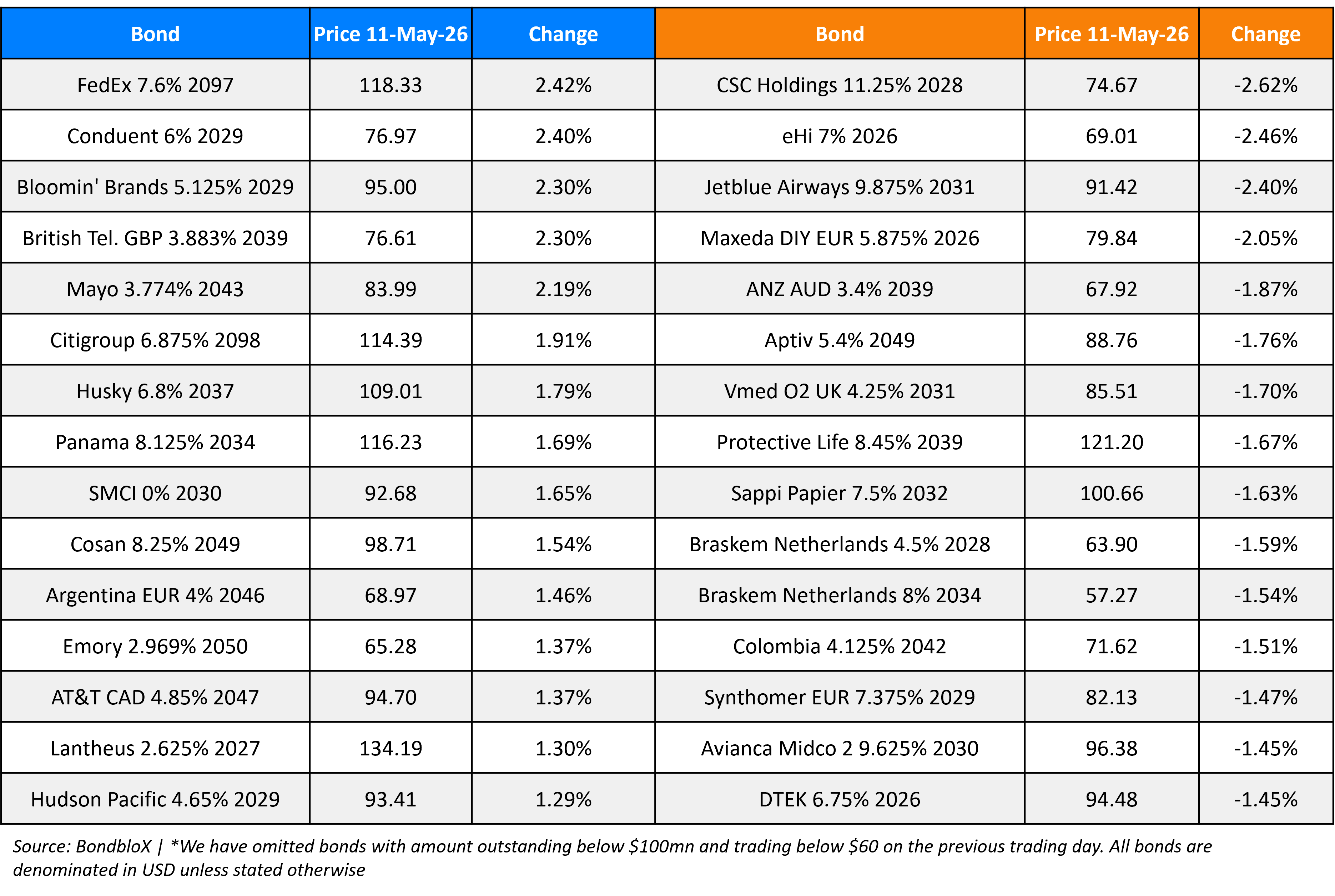

Top Gainers and Losers- 11-May-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.