We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

Goldman, Santander, NatWest and Other Price Bonds

May 28, 2026

US Treasury yields rose by 4-7bp across the curve. Mixed signals continue regarding the progress towards a US-Iran agreement, with Brent crude prices staying volatile. US President Donald Trump said that Iran “wants to make a deal” but the US was “not satisfied”. On the data front, the Conference Board Consumer Confidence Index reading for May came-in at 93.1, better than expectations of 92.0. The Richmond Fed Manufacturing Index came-in at 13, better than expectations of 4.

Looking at equity markets, the S&P and Nasdaq ended marginally higher. US IG CDS spreads and HY CDS spreads tightened by 0.2bp each. European equity markets ended in the green. European IG CDS spreads were 0.1bp tighter and Crossover spreads tightened by 1.5bp. Asian equity markets have opened lower this morning. Asia ex-Japan CDS spreads tightened by 2bp.

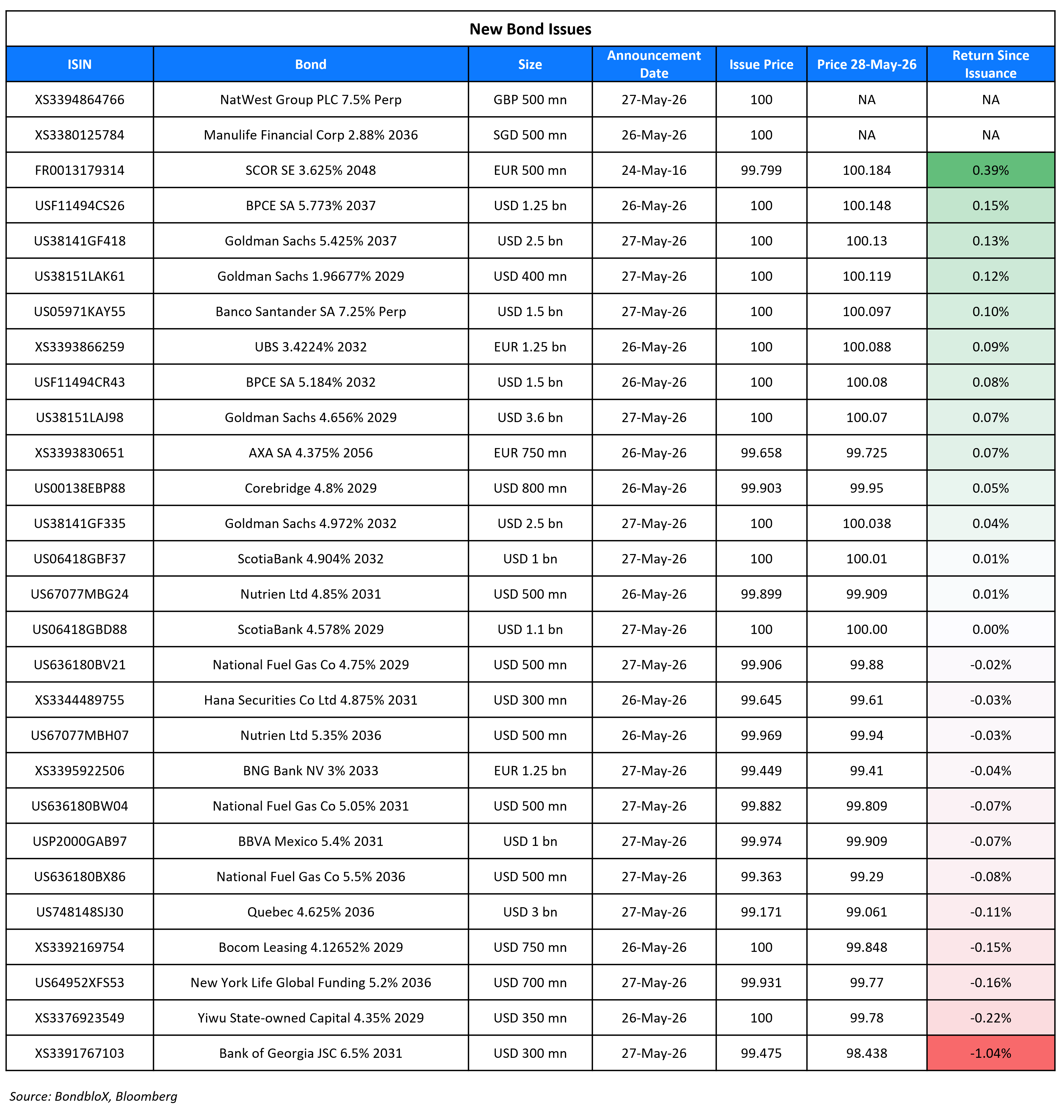

New Bond Issues

- StanChart $ PerpNC7 AT1 at 7.375% area

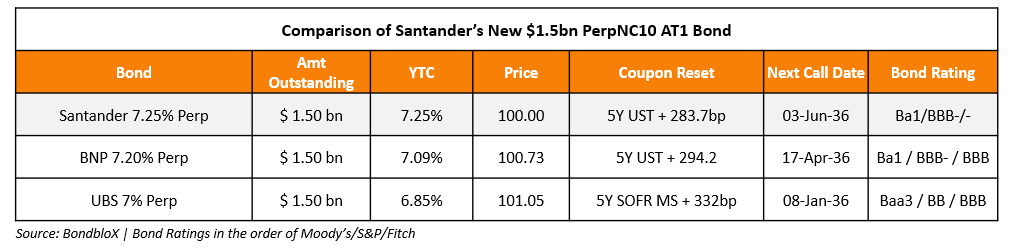

Santander raised $1.5bn via a PerpNC10 AT1 bond at a yield of 7.25%, 50bp inside initial guidance of 7.75% area. The junior subordinated note is rated Ba1/BBB-. If not called by 3 June 2036, the coupon will reset to the US 5Y Treasury yield plus 283.7bp. Below is a table comparing Santander’s new issuance with its peers.

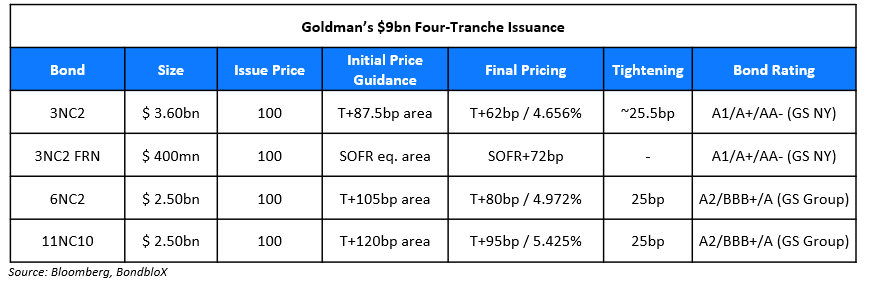

Goldman Sachs raised $9bn via a four-trancher. It raised:

Proceeds will be used for general corporate purposes.

NatWest raised £500mn via a PerpNC10 AT1 bond at a yield of 7.5%, ~56.25bp inside initial guidance of 8.00-8.125% area. The junior subordinated note is rated Baa3/BBB (Moody’s/Fitch). If not called by 3 December 2036, the coupon will reset to the prevailing UK 5Y Gilt yield plus 264.8bp.

Manulife Financial raised S$500mn via a 10NC5 Tier-2 bond at a yield of 2.88%, 32bp inside initial guidance of 3.20% area. The subordinated note is unrated. Proceeds will be used for general corporate purposes, including investment in subsidiaries and potential future redemptions of existing securities.

Scor raised €500mn via a 30NC10 Tier-2 bond at a yield of 4.51%, 25bp inside initial guidance of MS+175bp area. The subordinated note is rated A3. Proceeds will be used for general corporate purposes, including the financing of the notes under its concurrent tender offer.

BPCE raised $2.75bn via a two-trancher. It raised $1.5bn via a 6NC5 bond at a yield of 5.184%, 25bp inside initial guidance of T+125bp area. It also raised $1.25bn via a 11NC10 bond at a yield of 5.773%, 27bp inside initial guidance of T+155bp area. The senior non-preferred notes are rated Baa1/BBB+/A. Proceeds will be used for general corporate purposes.

Scotiabank raised $2.1bn via a dual-trancher. It raised $1.1bn via a 3NC2 bond at a yield of 4.578%, 25bp inside initial guidance of T+80bp area. It also raised $1bn via a 6NC5 bond at a yield of 4.904%, 27bp inside initial guidance of T+100bp area. The senior unsecured notes are rated A2/A-/AA-. Proceeds will be used for general corporate purposes.

Hana Securities raised $300mn via a 5Y bond at a yield of 4.956%, 33bp inside initial guidance of T+110bp area. The senior unsecured note is rated A- by S&P. Proceeds will be used for general corporate purposes.

Bocom Financial Leasing raised $750mn via a 3Y FRN at SOFR+48bp, 57bp inside initial guidance of SOFR+105bp area. The senior unsecured note is rated A2/A (Moody’s/Fitch). Proceeds will be used for general corporate purposes. Bank of Communications Financial Leasing Co. Ltd. 2 is the Keepwell and asset purchase deed provider.

Rating Changes

- Fitch Upgrades YPF to ‘B-‘; Outlook Stable

- Fitch Upgrades Puma Energy to ‘BB+’; Outlook Stable

- AngloGold Ashanti PLC Upgraded To ‘BBB-‘ On Sustained Cost Discipline And Strong Credit Metrics; Outlook Stable

- Moody’s Ratings upgrades CrowdStrike’s rating to Baa2; Outlook stable

- Moody’s Ratings upgrades Cirsa to Ba3; outlook stable

- Interpipe Holdings PLC Upgraded To ‘CCC+’ On Repayment Of Notes; Outlook Stable

- NTT Downgraded To ‘BBB+’ On Delayed Financial Recovery; Outlook Stable

- Fitch Downgrades Whirlpool’s IDR to ‘BB-‘; Outlook Negative

- HSBC Outlook Revised To Positive On Strong Strategic Execution And Resilient Global Balance Sheet

- Moody’s Ratings changes Republic of the Congo’s outlook to positive from stable, affirms Caa2 ratings

Term of the Day: Regulation S

A Regulation S or Reg S bond is one that is issued in the international bond market and is usually cleared through Euroclear and Clearstream. These bonds cannot be sold in the US, except to qualified institutional buyers (QIBs) under the SEC 144A Rule. The 144A Rule, issued in 1990, modified a two-year holding period rule on privately placed securities by permitting (Qualified Institutional Buyer) QIBs to trade in these securities among themselves. Thus, a 144A bond, with a unique identifier, is privately placed to US based QIBs and usually clears through DTCC.

Talking Heads

On Fed Must Pivot to Inflation Fighting – Nohshad Shah, Citadel Securities

“Inflation, not the labor market is the greater risk. The Fed should take note and adjust their stance soon, lest they get behind the curve… bond market is awakening to the reality of a hot economy with risks of a classic demand-induced inflation process”

On Warning of Oil Shock Impact on Entire Inflation Regime – Kazuo Ueda, BOJ Governor

“Japan’s experience shows that oil price shocks are never just oil price shocks. They are tests of the entire inflation regime… we are actually facing a fifth oil price shock… boundary between temporary and persistent inflation is not mechanical”

On Leveraged Hedge Fund Bets Risking Bond Market Instability – ECB

“Their leveraged positions may have to be unwound quickly if bond prices react sharply to geopolitical or risk sentiment shocks, for instance… The growing presence of more price-sensitive investors like hedge funds in euro area sovereign bond markets could amplify any abrupt repricing of sovereign risk”

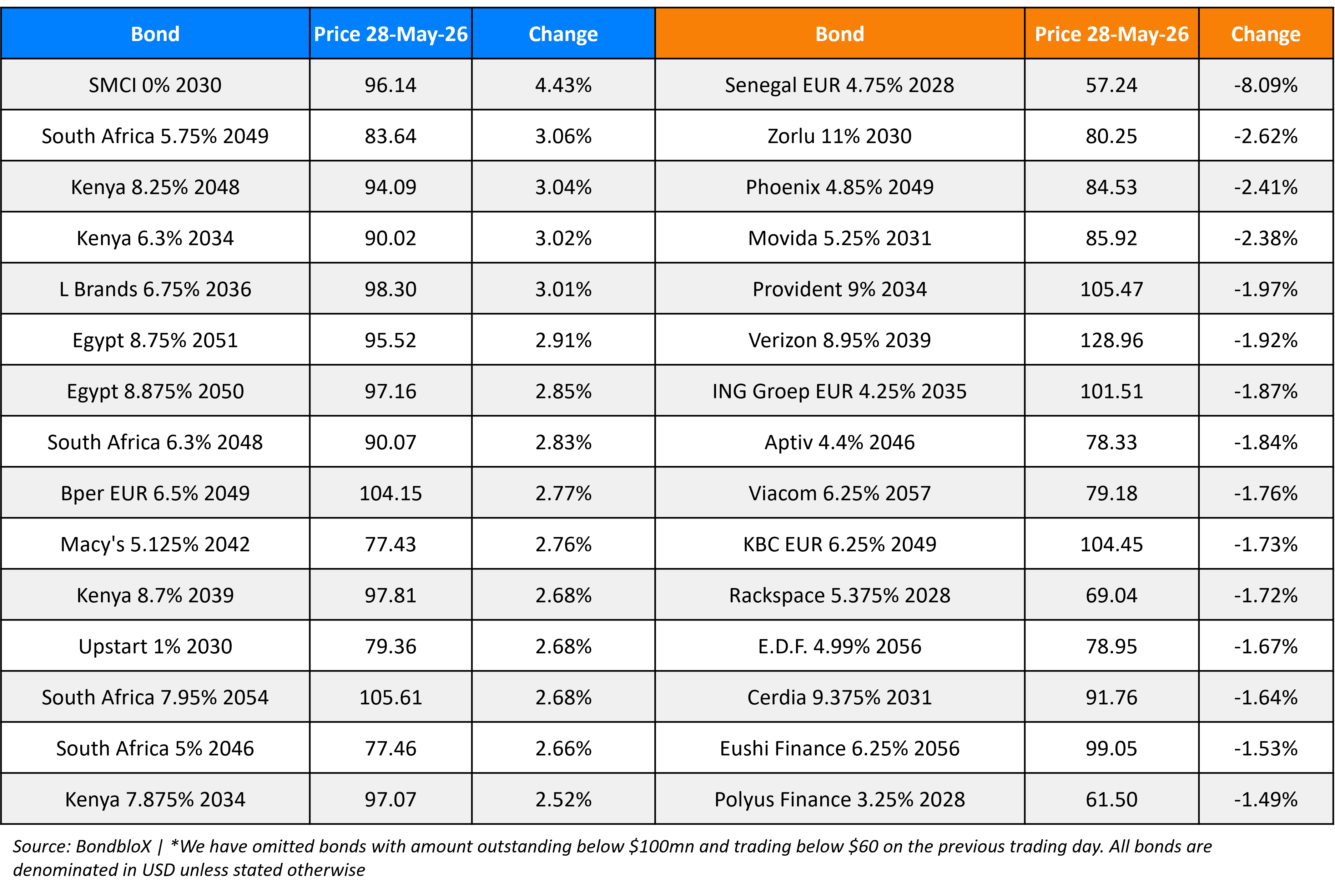

Top Gainers and Losers- 28-May-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.