We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

BNI Launches $ Perp; BNP Prices $ AT1 at 7.2%

April 15, 2026

US Treasury yields eased further by another 3-4bp as the risk-on sentiment continued. A potential second round of US-Iran talks is on the cards, alongside Israel and Lebanon agreeing to hold diplomatic talks for the first time since 1993. On the data front, US Headline PPI for March grew by 4.0% YoY, softer than the surveyed 4.6%. The Core PPI print grew by 3.8%, softer than the surveyed 4.1%.

Looking at US equity markets, the S&P and Nasdaq ended 1.2% and 2% higher respectively. US IG CDS spreads tightened by 0.5bp while HY CDS spreads were 5.5bp tighter. European equity indices ended higher too. The iTraxx Main CDS spreads tightened by 2.7bp and Crossover spreads were 14.5bp tighter. Asian equity markets have opened in the green this morning. Asia ex-Japan CDS spreads were 1.8bp tighter.

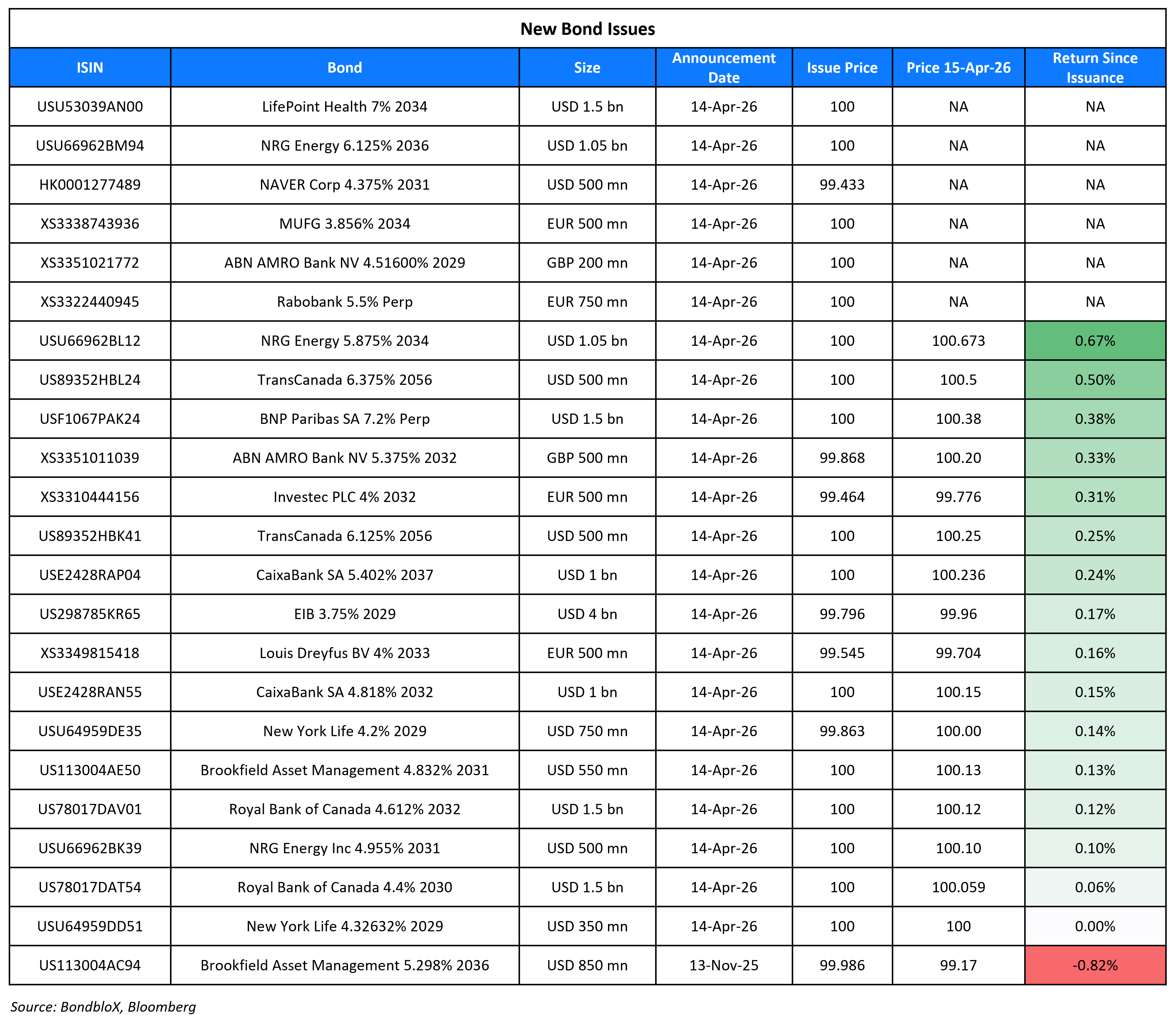

New Bond Issues

-

Bank Negara Indonesia $ PerpNC5.5 at 7.5% area

-

Sompo $ 11NC10 at T+145bp area

-

CIMIC $ 10Y at T+120bp area

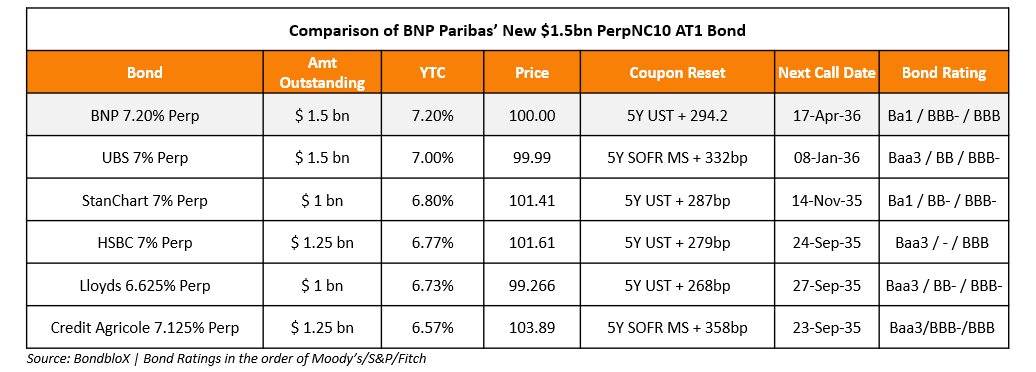

BNP Paribas raised $1.5bn via a PerpNC10 bond at a yield of 7.20%, ~48.75bp inside initial guidance of 7.625-7.75% area. The junior subordinated note is rated Ba1/BBB-/BBB. If not called by 17 April 2036, the coupon will reset to the US 5Y Treasury yield plus 294.2bp. Proceeds will be used for general corporate purposes. Below is a comparison of the latest issuance with its peers.

CaixaBank raised $2bn via a two-tranche deal. It raised $1bn via a 6NC5 bond at a yield of 4.818%, 30bp inside initial guidance of T+125bp area. It also raised $1bn via a 11NC10 bond at a yield of 5.402%, 30bp inside initial guidance of T+145bp area. The senior non-preferred notes are rated Baa1/BBB+/A-. Proceeds will be used for general corporate purposes.

Rabobank raised €750mn via a PerpNC7.5 bond at a yield of 5.5%, 50bp inside initial guidance of 6.0% area. The junior subordinated note is rated Baa3/BBB (Moody’s/Fitch),and received orders of over €3.2bn, 4.3x issue size. If not called by 29 December 2033, the coupon will reset to the EURIBOR 5Y ICE Swap Rate plus 257.8bp.

Royal Bank of Canada raised $3bn via a two-tranche deal. It raised $1.5bn via a 4NC3 bond at a yield of 4.4%, 25bp inside initial guidance of T+90bp area. It also raised $1.5bn via a 6NC5 bond at a yield of 4.612%, 25bp inside initial guidance of T+100bp area. The senior unsecured notes are rated A1/A/AA-. Proceeds will be used for general corporate purposes.

NRG Energy raised $500mn via a 5Y bond at a yield of 4.955%, 32bp inside initial guidance of T+140bp area. The senior secured first lien bond is rated Baa3/BBB-/BBB-. Proceeds along with those of its New Term Loan B, will be used to pay for the notes under its tender offer and the remainder for general corporate purposes.

TransDigm raised $500mn via a tap of its 6.125% 2034s at a yield of 6.066%. The deal was upsized from the intial $250mn. Proceeds, together with the net proceeds of the additional Tranche N Term Loans, will be used to fund the purchase of its Stellant Acquisition and for general corporate purposes.

MUFG raised €500mn via an 8NC7 bond at a yield of 3.856%, ~32.5bp inside initial guidance of MS+125/130bp area. The senior unsecured note is rated A1/A-/A-.

TransCanada Pipelines raised $1bn via a two-tranche deal. It raised $500mn via a 30.5NC5.25 bond at a yield of 6.125%, 50bp inside initial guidance of 6.625% area. It also raised $500mn via a 30.5NC10.25 bond at a yield of 6.375%, 50bp inside initial guidance of 6.875% area. The junior subordinated notes are rated Baa3/BBB-/BBB-. Proceeds will be used to partially fund the redemption of its subordinated trust note, to reduce other debt, and for general corporate purposes.

New Bonds Pipeline

- SoftBank Plans $/€ bonds

- Korea Expressway $ 3Y/5Y bond bond

Rating Changes

- Fitch Upgrades UBS Group to ‘A+’; Outlook Stable

- Fitch Upgrades Shriram Finance to ‘BBB-‘; Off Ratings Watch Positive; Outlook Stable

- Fitch Downgrades Amaggi’s IDR to ‘BB-‘; Outlook Negative

- Bombardier Inc. Outlook Revised To Positive On Improving Credit Metrics And Strong Operational Performance

- Moody’s Ratings changes Kohl’s outlook to positive; affirms B2 CFR

Term of the Day: Panda Bonds

Panda bonds are renminbi denominated notes sold by a non-Chinese issuer in onshore China. The first of its kind was issued by the IFC and ADB in 2005. While these bonds attract Chinese investors, they have also gained traction among international investors. It also helps issuers diversify investor bases and reduce currency risk.

Talking Heads

On Bond investors targeting steeper US yield curve on bets for slower growth, more debt issuance

Padhraic Garvey, ING New York

“The back end of the curve has issues with inflation expectations and on the front end, we’re not expecting the Fed to react by hiking rates”

Vishal Khanduja, Morgan Stanley Investment Management

“As yield curves are normalizing, you will see the probability of cuts go higher”

Guneet Dhingra, BNP Paribas

“In an escalation scenario where growth concerns offset inflation fears, front-end yields do not rise, while the long end starts to rise because deficit concerns start to build”

On Iran War Lifting Africa Debt Costs That Have Surged Since Pandemic

Lei Zhu, Fidelity International

“As Middle-East tensions periodically disrupt US dollar credit markets, the Hong Kong dollar stands out as a stable, conflict‑free, US dollar‑linked currency, attracting diversification‑driven demand… Although Hong Kong dollar bonds are not absolutely risk-free, they should be seen as a defensive safe‑haven asset”

Oliver Greer, Standard Chartered Bank

“Demand for high quality Hong Kong dollar denominated assets from bank investors remains particularly strong, given their historically low loan-to-deposit ratios and the overall stable backdrop”

On Traders Targeting Bond Market Rally on Iran War ‘Tone Change’

Ian Lyngen, BMO Capital Markets

“The extent to which the tone change is able to hold is unquestionably a wild card and investors are cognizant that a swift reversal could easily be a social media post away”

Raghav Datla, Citigroup Global Markets

“Until there’s clarity on the macro perspective, you’re not going to see those flows coming in”

Top Gainers and Losers- 15-Apr-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.